Oil companies could scale back ambitious plans to expand wind and solar-power capacity, and electricity and gas-supply portfolios, we believe, if returns disappoint. Oil and gas activities have higher returns than renewable projects, in which utilities' lower funding costs give them an edge over oil majors when bidding for green projects.

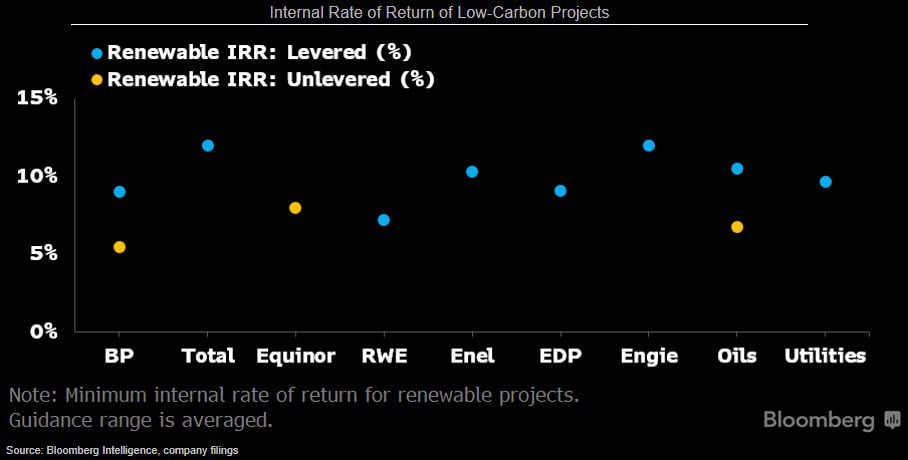

Integrated oil companies may scale back ambitious plans for investing in renewables and low-carbon-energy projects amid mediocre returns. It's difficult to compare the internal rate of return (IRR) targets of green projects between companies because some include leverage and gains from disposals.

Overall, the IRR expected by oil companies is higher than those of rival utilities, despite the latter group having lower financing costs, greater experience in developing wind and solar projects and larger renewable portfolios, and thus benefiting from greater economies of scale.

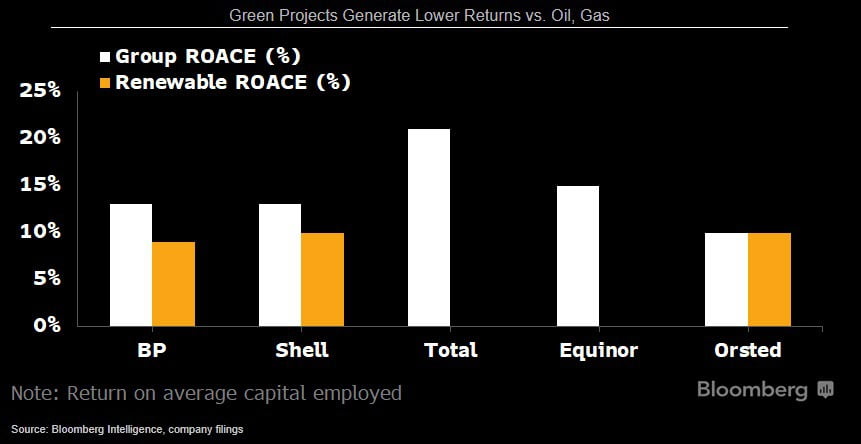

Core oil and gas business will continue to account for the majority of oil majors' capital spending, though a relatively small -- but growing -- proportion of annual budgets are being put toward energy-transition projects. That's because companies expect to generate a higher return on average capital employed (ROACE) from their core operations compared with green projects. Similarly, the overall ROACE of oil companies, including BP, Shell, Total and Equinor, exceeds that of wind and solar developers such as Orsted.

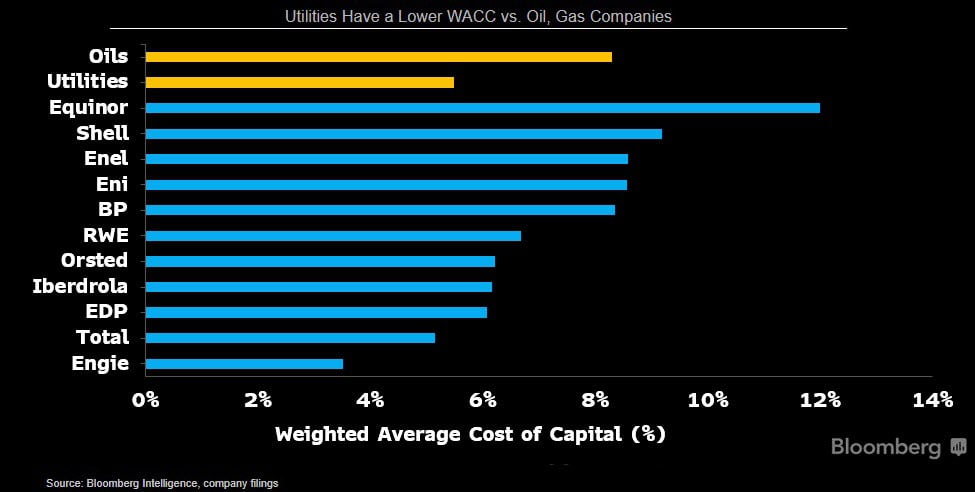

Lower funding costs give utilities an edge over oil rivals when bidding for green projects and may enable the former to potentially generate higher returns from wind and solar projects. The gap in the weighted average cost of capital (WACC) between utilities and oil majors may widen further, we believe, both in terms of cost of debt and equity.

On the debt side, utilities' greater exposure to renewables and the lower risk of stranded assets help them to issue bonds at lower rates than big oil rivals. The increased focus of investors on climate and sustainability may also lead to higher cost of equity for oil and gas companies, who face the proliferation of ESG-focused ETFs and the increased scrutiny from money managers, such as Blackrock, who make their support conditional on companies' progress on climate issues.