While Big Oil aims to expand its renewables portfolio aggressively, we remain more skeptical over the industry's ambitious plans to grow its end-customer base in electricity and gas. The bigger threat for utilities in their core retail business will more likely be non-oil new entrants.

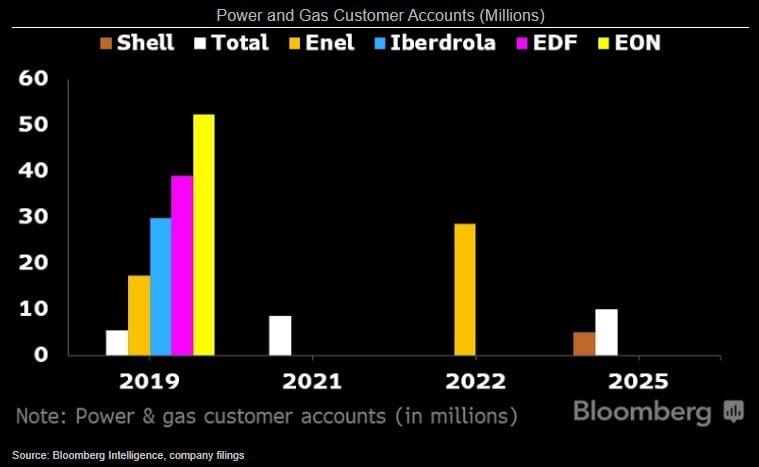

Selling electricity, natural gas and energy services directly to businesses and households is a strategic growth area for oil majors. Shell and Total plan to grow their portfolios to 5 million and 10 million customers respectively by 2025. While this would still be well below the number of customer accounts held by EON, EDF, Iberdrola and Enel, it would represent a more than 6x increase for Shell and a near-doubling for Total vs. 2019. Most of that growth would likely come from acquisitions rather than organic sources. Since 2018, Total has agreed to purchase 2.5 million customer accounts from utility EDP, Repsol bought Viesgo's 0.7 million-account portfolio, and Shell acquired First Utility, serving 0.8 million households and businesses.

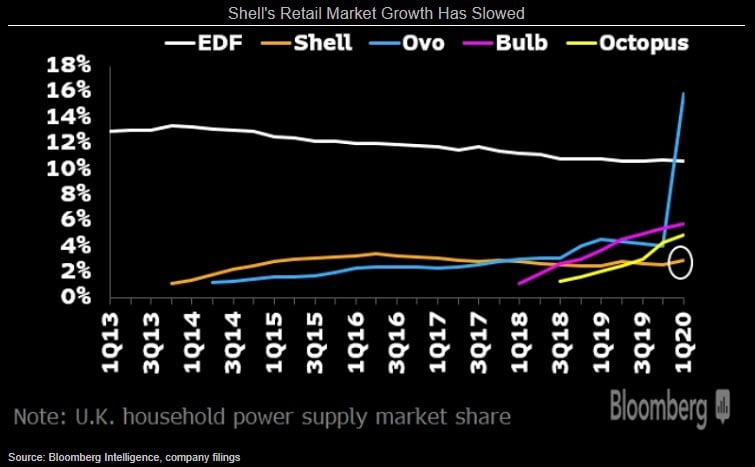

Despite its push into renewables and low-carbon power generation, Big Oil may fail to challenge utilities in the battle for residential customers. Shell has been unable to grow its market share in the U.K. since acquiring First Utility in 2018. The main threat for incumbent utilities may come from new, challenger brands. Focusing on innovation and cost-efficiency has helped Bulb, Octopus and Ovo Energy to overtake Shell and narrow their market-share gap with incumbent utilities EDF and Centrica in supplying gas and power to U.K. households.

Energy retail is a low-margin business and this may prompt oil companies to scale back their plans if they fail to achieve solid, organic growth while maintaining adequate returns.