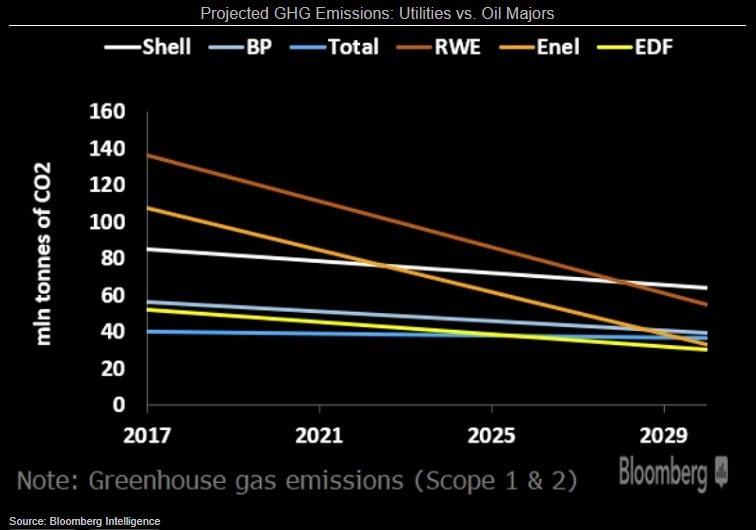

It will take oil & gas companies significantly longer to decarbonize than most European utilities, in our view. Mature wind, solar and battery storage technologies will be the key route for utilities to reach their climate-neutrality goals. Until hydrogen and carbon capture and storage become economical, oil companies will focus on carbon sinks and increasing revenue shares in gas and renewables.

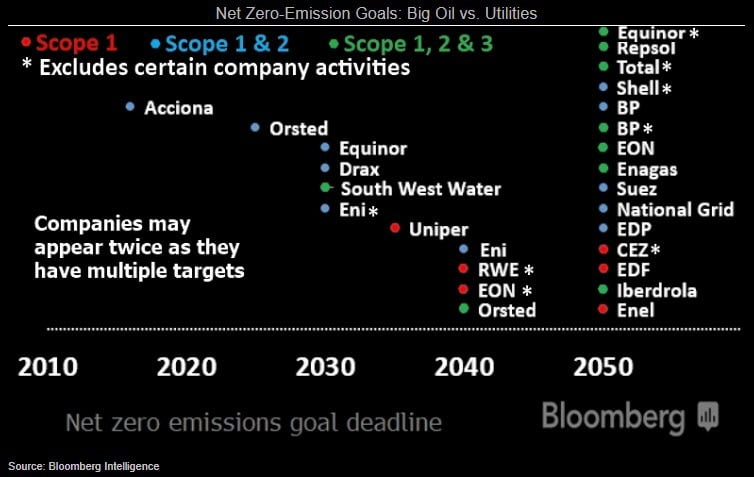

European utilities tend to have more-ambitious climate neutrality goals compared with oil & gas companies. Among utilities, Acciona, Orsted and Drax stand out amid ambitious goals. By contrast, Engie, Naturgy and Fortum have yet to adopt net zero-emission goals. Within European oil companies, Repsol, Energean and Eni appear to have the most-ambitious targets, while BP leads among the oil majors. Oil companies are also more likely than utilities to exclude their certain activities from net-zero targets by limiting them to certain geographies (Equinor to Norway, Total to Europe) or parts of the value chain (upstream for Eni's 2030 goal, power generation but not heat for CEZ).

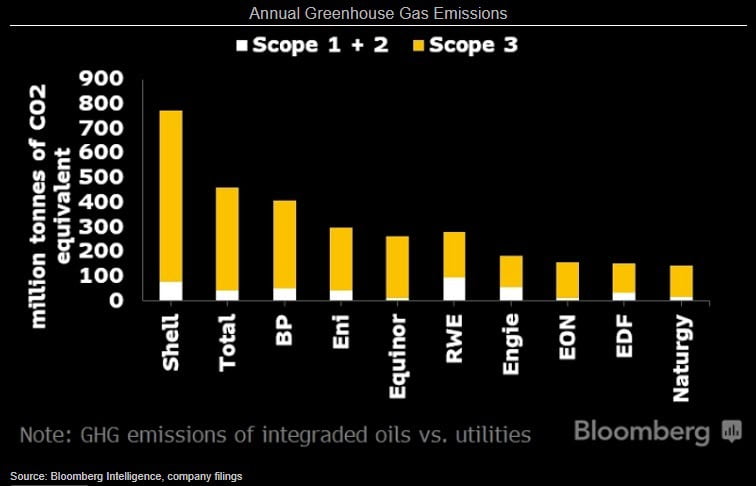

The combined annual direct greenhouse emissions (scope 1 and 2) of the five largest integrated oil companies in western Europe (Shell, Total, BP, Eni and Equinor) are broadly comparable to the five biggest utility emitters in the region (RWE, Engie, EON, EDF and Naturgy). Yet these oil companies have 2.4x higher indirect (scope 3) emissions than utilities. The gap in total emissions of the two industries may widen further in 2020-21 as a plunge in electricity demand due to the pandemic and deteriorating economics of coal-power vs. gas-fired generation could help utilities further reduce the emission intensity of their assets, in our view.

Power utilities as well as water and waste management companies may be able to decarbonize faster than oil & gas producers (especially smaller, independent players), refiners and gas-grid operators, particularly when it comes to reducing scope-3 emissions. For electricity generators suppliers, the main focus will be on replacing legacy coal, oil and gas-fired generation with renewables and battery storage, and helping customers improve energy efficiency. Hydrogen and biomethane would be the key lever for gas-focused utilities, including Enagas, Snam, National Grid and Engie. Carbon capture, utilization and storage (CCUS) would be of little importance for most of Europe's large, listed utilities. Exceptions are Drax, Uniper and EPH.

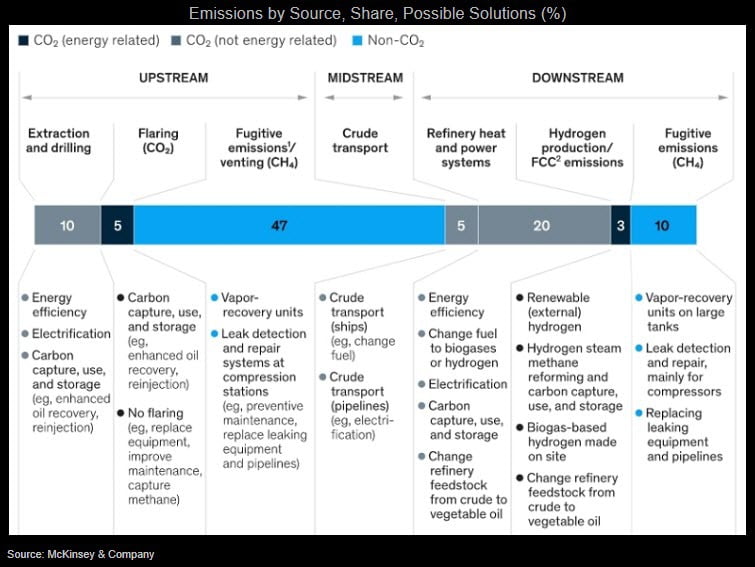

Carbon capture, utilization and storage, if it ever becomes economical, and hydrogen, once it's commercialized, would be game-changers for oil & gas companies (BP, Shell, Equinor) seeking to reduce emissions. For the time being, the key levers for oil companies to reduce their emissions footprint would be through acquiring carbon offsets (reforestation, afforestation and forests conservation), increasing their shares in gas, renewables and biofuels vs. crude oil in the energy mix, and reducing carbon leakage.

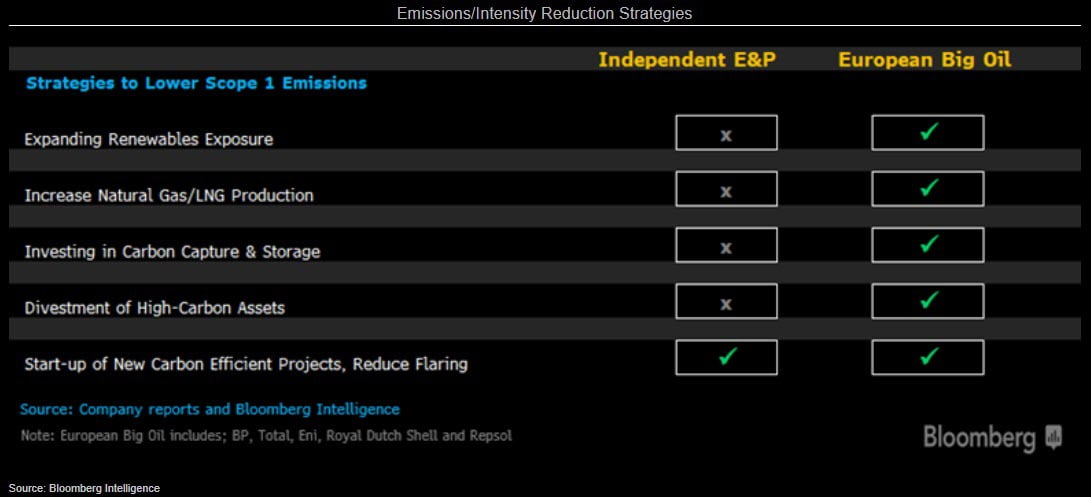

Independent E&Ps' ability to curtail greenhouse-gas emissions remains significantly constrained, in our view, particularly for Scope 3, given the sector's primary objective of maximizing hydrocarbon recovery. Strategies available to the companies are largely limited to improving efficiency and reducing flaring, especially for those with a legacy portfolio bias. With a new generation of low-emission projects, Lundin is among the lowest global emitters and has set a net-zero target (Scope 1-2), along with Premier Oil and Kosmos.

Conversely, oil majors have a more extensive toolkit to reduce emissions, including changing product mix toward gas/LNG, divestment of carbon-intense assets (oil sands, legacy offshore) and investment in renewables, carbon capture and natural carbon sinks.