Utilities shouldn't fear the foray of European oil majors into power. The pie is big enough for both, we believe, while lower financing costs give utilities an advantage. Big Oil's green push makes utilities potential M&A targets, but also provides an outlet for those seeking to divest renewables projects to recycle capital, boost returns and reduce risk.

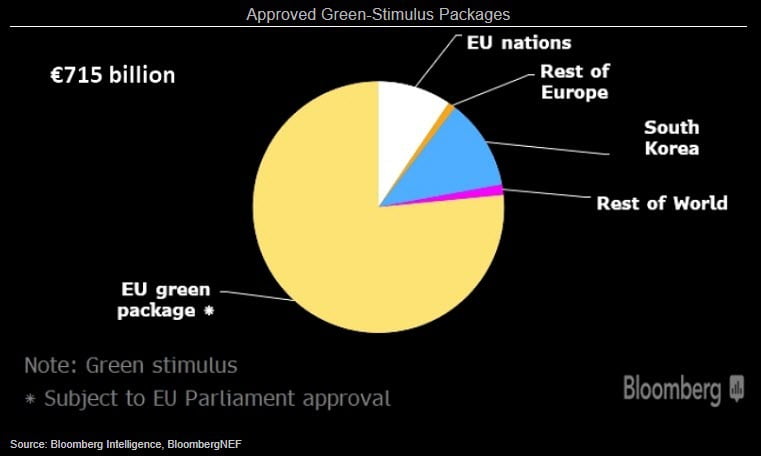

The entry of oil companies into renewables and e-mobility shouldn't perturb utilities as these markets are more than big enough for both groups to coexist, in our view. Global green-stimulus measures to help the economies hurt by the Covid-19 pandemic will make the renewable pie even bigger, we believe. So far, green-recovery plans by individual European countries (led by France and Germany) already exceed 75 billion euros. On top of that, the EU has approved a plan to invest more than 500 billion euros in green projects through 2027. In the U.S., presidential candidate Joe Biden has promised a $2 trillion climate plan over four years if he wins the November election.

Europe's integrated oil companies will have to resort to acquisitions to reach their aggressive growth goals for renewable-generation capacity and the number of power and gas-retail customers. Top integrated utilities such as Enel and Iberdrola may be too large even for Big Oil to absorb, while Orsted, RWE, SSE and EDP may be more realistic targets. Yet we believe oil companies will instead focus on acquiring small and midsize wind and solar developers, such as Falck Renewables, Solaria Energia, Neoen, Voltalia and Encavis. Scatec Solar, where Equinor has accumulated a 15% stake, could be another candidate.

In energy retail, Centrica's declining market capitalization and stabilizing market share increasingly make it a target for Big Oil, in our view.

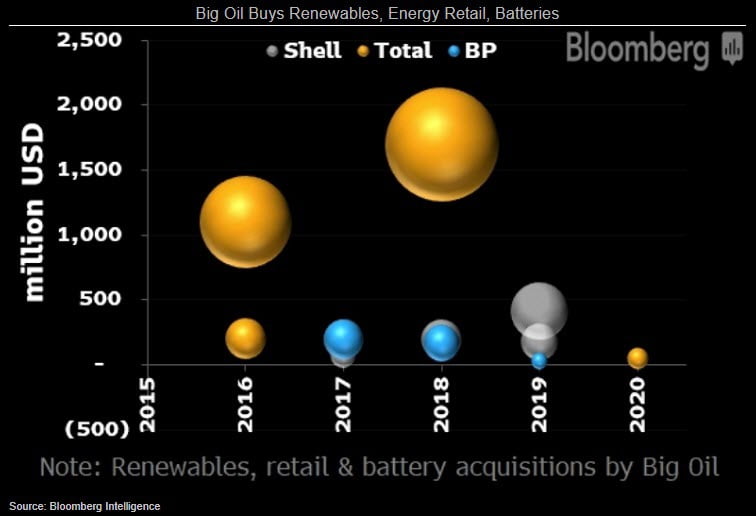

Among European oil majors, Total and Shell have been more active than BP in acquiring renewables (Silicon Ranch, Lightsource), energy retail (First Utility, ERM Power, Direct Energie, Lampiris) and EV-charging and battery-storage (Saft, Chargemaster, Sonnen) businesses in the past five years, our calculations show.

Dealmaking by value peaked in 2018, then troughed in 2020 as Covid-19 and the crude-price crash prompted oil companies to curb spending. We expect M&A to recover in the next year or two as the commodity-market shock wears off.

Oil majors' push into renewables is a significant but manageable threat to utilities, in our view. The groups will increasingly compete at green-power auctions. Still, SSE and other generators welcome efforts by Big Oil to expand renewable capacity because it pushes up valuations for wind and solar assets, which many utilities routinely sell to recycle capital and boost returns.

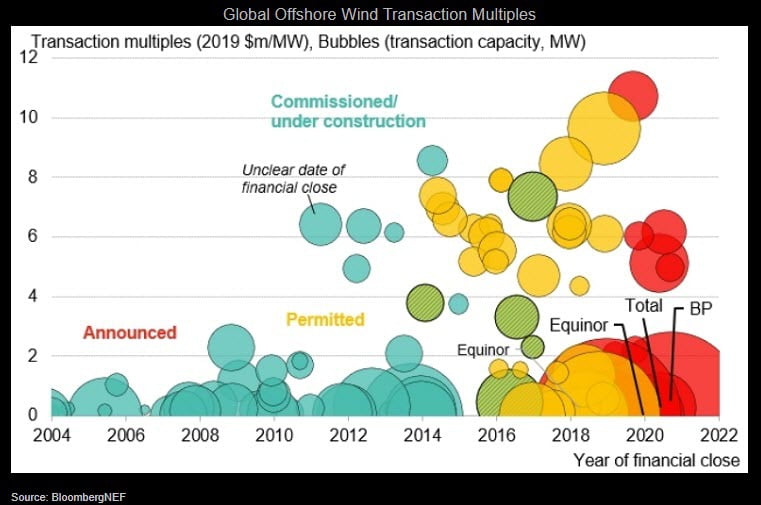

Yet recent offshore-wind deals suggest that large integrated oil companies don't tend to overpay for such assets.

Wind and solar developer Forestalia sold its renewable assets in Spain to BP and Repsol.

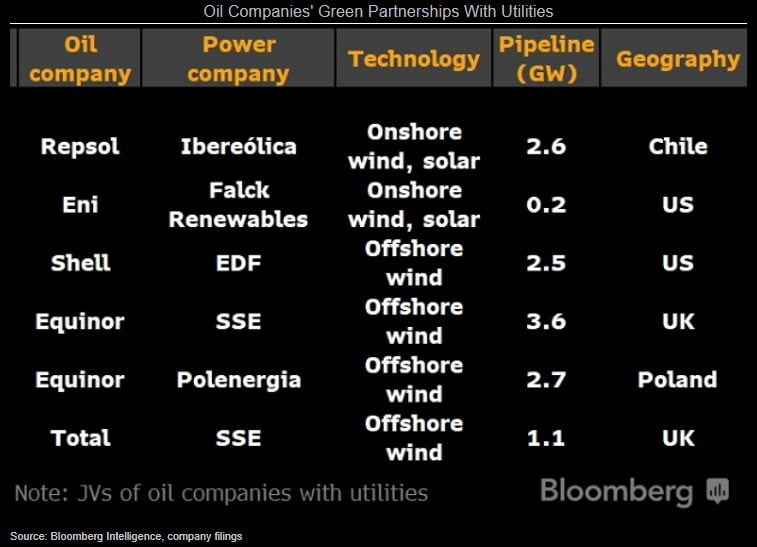

Oil majors will both compete and collaborate with utilities in deploying wind farms and solar, helping the former to enter new geographies and accelerate the buildout of renewable capacity. Unlike infrastructure funds (which have low cost of capital), oil companies may have a deeper expertise in offshore wind, hydrogen, power trading and optimization and greater appetite for risk when entering new regional markets or backing early-stage projects.

Repsol, Eni and Equinor have bought into wind-and-solar project pipelines of Ibereolica in Chile, Falck Renewables in the U.S. and Polenergia in the Baltic Sea. Shell and EDF jointly acquired lease rights to develop offshore wind off the coast of New Jersey. Total and Equinor are SSE's partners in U.K. offshore-wind projects.