With a few exceptions (Orsted, ERG), oil companies have been relative latecomers to green transition. This and the recent oil-price crash amid COVID-19 has helped the valuation, market capitalization and dividend yield of European utilities surpass oil peers. The transformation of oil majors into energy majors may weaken their share-price link with crude.

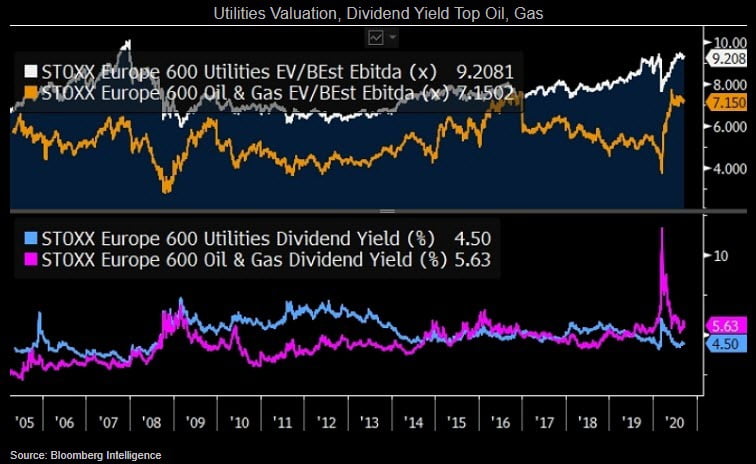

The valuation premium of utilities over oil and gas producers, refiners and transporters in Stoxx Europe 600 index has widened since the start of 2010. Utilities now trade at a 9.2x forward EV-to-Ebitda multiple vs. 7.2x for oil and gas companies, which are latecomers in green transitioning.

Moreover, historically, oil and gas companies were known for paying high dividends. Yet, the oil price crash and COVID-19 pandemic have triggered announcements of dividend cuts and buyback freezes by oil majors while utilities' dividends have been more resilient.

The green-transformation strategy adopted by many of Europe's listed utilities, as well as the oil-price crash have helped many of Europe's large, integrated utilities narrow the gap and even overtake oil and gas companies in the region on market capitalization. A decade ago, the equity value of BP and Shell was 3.4-3.8x higher than that of Enel and Iberdrola.

Today, Enel and Iberdrola have already overtaken BP (as well as Eni and Equinor) by market cap and Shell's lead over these two largest European utilities has shrunk to just 15-30% today.

The combined market cap of oil and gas companies in the Stoxx Europe 600 and S&P 500 indexes has fallen behind that of defensive utilities, mirroring the 2007-08 financial crisis. Declining demand and energy prices have damaged oil and gas producers' margins and valuations.

In the short term, utilities may be unable to hold their market lead once the COVID-19 headwinds fade and energy markets rebound after the price crash. In the longer run, utilities' greater focus on ESG, energy transition and electrification may help them outperform oil and gas producers, which face the risk of stranded assets.

Two out of BP's three main future-demand scenarios indicate that global oil demand has already peaked.

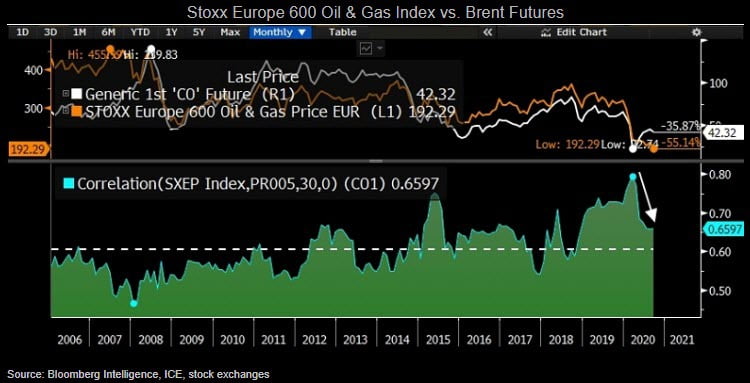

The strategy of oil majors to transition themselves into broader energy majors may weaken the link between their shares and the price of the crude-oil markets. Integrated oil and gas companies plan to become broader energy companies by expanding into renewables and increasing the share of gas in their asset portfolio in order to reduce their emission intensity. The correlation between crude oil futures and the share prices of oil and gas companies in the Stoxx Europe 600 index has declined since March, yet remains well above the 15-year average.