To download a PDF version, click on the Contents menu on the top left and select "Download PDF" on the bottom right.

The concept of a wheel arises from two key decisions traders make when routing an equity order to a broker-dealer (usually an algorithmic broker-dealer, but the framework extends to any broker-dealer). The first decision relates to an execution strategy, i.e., how a given order should be executed. This decision usually requires a slew of unstructured inputs including portfolio manager instructions, market conditions, order characteristics, accounts on the order, among others. The other decision relates to the specific broker-dealer that the order is directed to, i.e., which broker-dealer should receive the order.

The opportunity to randomize presents itself in the broker selection process. It’s the opportunity to examine the value each broker-dealer is adding to the trading process. Post-trade analysis of broker-dealer transaction costs will provide more insights if the dataset has been carefully created to measure differences between brokers, instead of analyzing order flow that has been directed ad hoc. A crude analogy is a medical trial performed to establish the efficacy of a drug. A placebo or an alternative treatment allows health experts to determine if a given drug or treatment is effective. An algo wheel allows trading desks to randomize order flow between a set of brokers and set up a controlled trial to evaluate broker-dealers. This approach allows the wheel framework to develop into a powerful method of streamlining execution across the entire desk’s order flow.

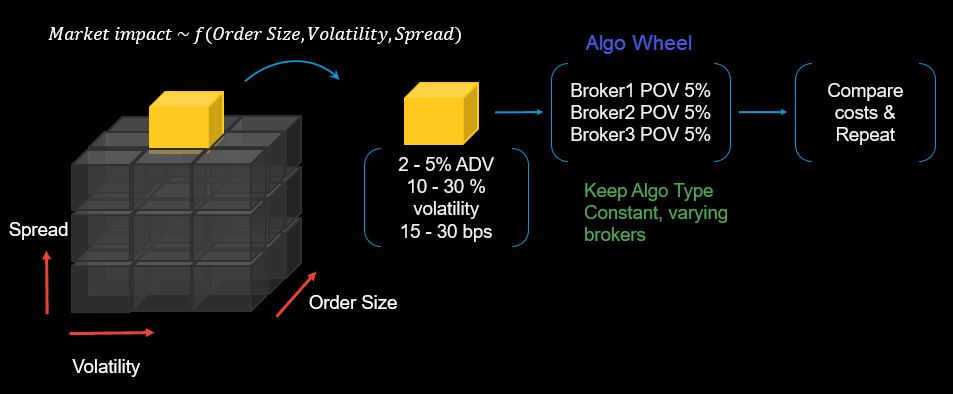

The illustration below shows an algo wheel and how to create a simple wheel for comparing three brokers with a standard algorithm known as ”participation of volume,” or POV. In this use case, a POV strategy has been assumed as the execution strategy for all orders. In Figure 1, a portion of the desk’s order flow is sheared off (represented by the small cube) and sent to the wheel over a specific time period, say a quarter. This yellow cube represents order flow with similar market impact or performance against price benchmarks. Restricting orders to a wheel based on similar market impact numbers allows us to measure variability in the real variable of interest, i.e., broker-dealers. This is similar to, as an example, to comparing fuel efficiency of cars based on passengers — the car model and make would be kept the same while varying the number of passengers. At the end of the time period, the post-trade analysis tools can be used to compare costs across the three brokers to measure performance vs. transaction benchmarks like arrival price or volume-weighted average price (VWAP).

Figure 1