Bloomberg’s new Performance Wheel allows traders to select top broker-algorithms for their wheel. The idea is to use a larger Bloomberg dataset to kick-start the broker selection process for creating broker wheels. The new feature uses a sophisticated machine-learning model to analyze and predict broker-algorithm performance against various standard benchmarks. This feature allows traders to find and run trials on better performing broker-algorithms within and outside of their trading desk’s regular usage. Bloomberg extracts order characteristics from the trading desk’s order flow and displays algorithm performance using both the trading desk’s own flow and Bloomberg-wide data for all available broker-algorithms on our platform.

The key model underlying this product predicts market impact of broker-algorithms based on:

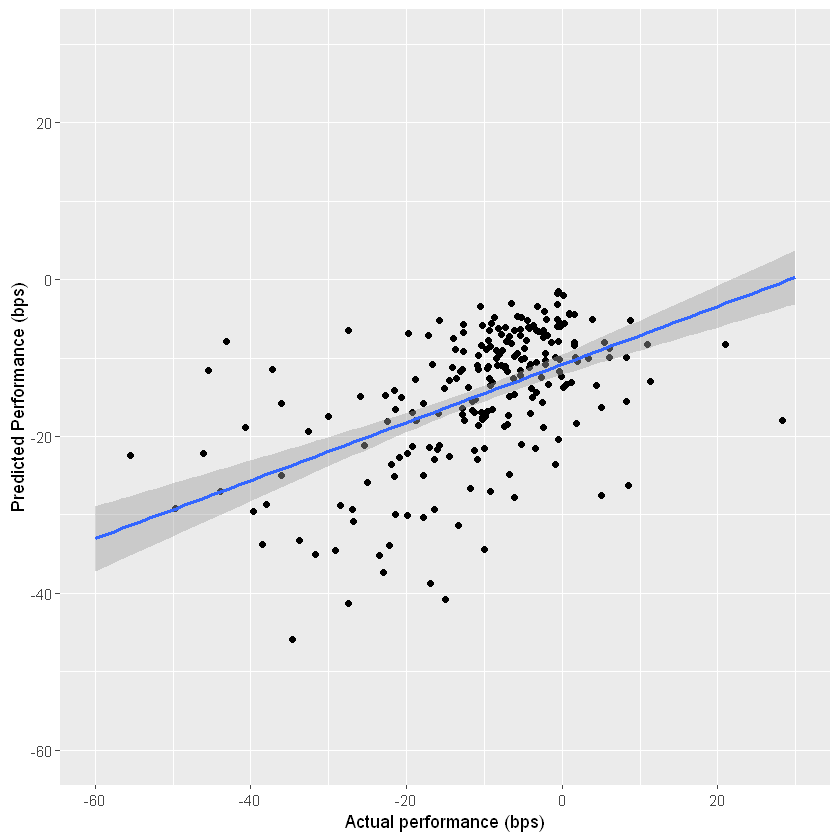

A unique, large internal dataset allows us to tease out differences between different broker-algorithms within U.S., EMEA and Asia. Clean datasets of broker-algorithm performance are especially difficult to find given that plenty of human intervention is possible while trading. Bloomberg makes sure to have large and pristine samples on individual algorithm performance across individual regions and order flow characteristics. The model is validated using out-of-sample data on broker-algorithms and their actual realized costs. We find promising evidence of the model being able to predict relative ranks for brokers and broker-algorithms. As shown in Figure 2, Predicted Performance (bps) is in line with Actual Performance (bps) observed in an out-of-sample dataset across a large swath of order flow. The model also predicts actual broker-algorithm performance on average within smaller groups of order size and participation rates (not shown here).

Figure 2