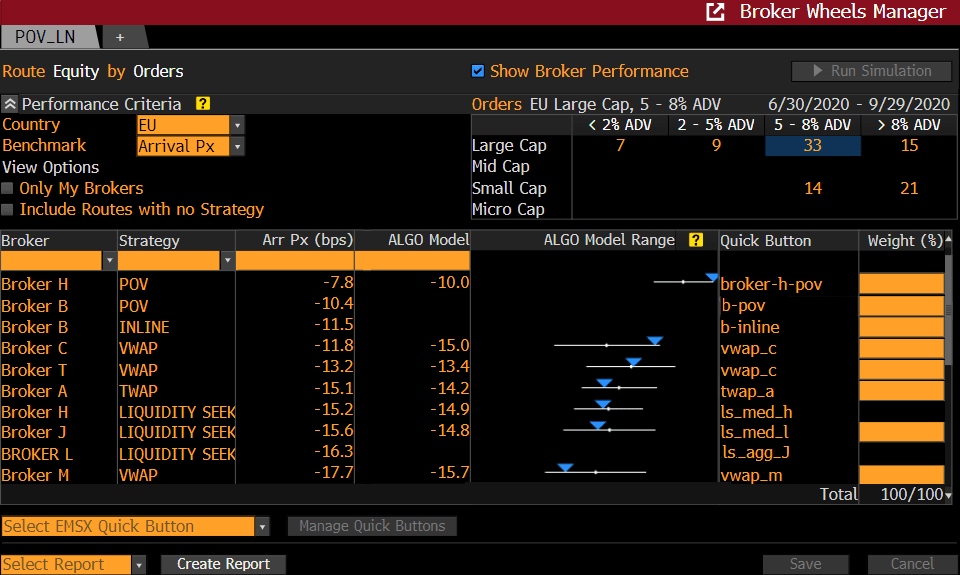

The first one uses their own experience with the brokers and the second, as explored above, leverages the wider Bloomberg dataset. Using extensive and detailed order routing history in our equities execution management system, EMSX, we compute and break down a client’s order flow into a grid (shown in Figure 3). This grid comprises rows of Market Capitalization and Percent of ADV categories. Each number in the category represents the percent of notional value the desk has traded over the last three months. For example, 33% of notional value of this order flow traded in Large Capitalization and 5-8% Average Daily Volume category.

For each category, aggregate client-specific order characteristics are computed. We then match Bloomberg model performance for each available broker-algorithm based on the order characteristics in the Bloomberg database. Each broker-algorithm’s predicted market impact cost is carefully matched to client flow based on average characteristics of category using average spread, historical volatility and percent of order size in relation to Average Daily Volume and participation rate of the orders. This allows a close comparison between the client’s own experience with a given broker-algorithm and the wider experience of all Bloomberg clients for the same broker-algorithm.

As an example, see Broker H & POV broker-algorithm pair in Figure 3, where there is an underperformance of –7.8 basis points vs. Arrival Price (column Arr Px, bps).The Bloomberg model (column ALGO Model) predicts performance to be centered around -10.0 basis points for the characteristics of the 33% of flow in the Large Cap-5-8% ADV category. The inset graphic with a white bar and a blue notch indicates how the two measures overlap and are meant to give clients an indication on how different their experience (blue triangle) with this broker-algorithm is compared with the larger Bloomberg universe (white bar range).

Figure 3

Clients can use this model to create a wheel for their execution strategies by identifying the best performing broker-algorithms to align with their in-house best execution processes. The last column in the screen below shows how weights for each broker-algorithm can be entered and saved to complete the creation of the broker wheel.

Using the performance wheel, traders can obtain a comprehensive dataset to ultimately lower implicit execution costs for end investors. To learn more about how to use this feature or be set up for this product, please get in touch with your Electronic Trading Sales representative.

Play the video to learn more about Bloomberg's equity automation solutions