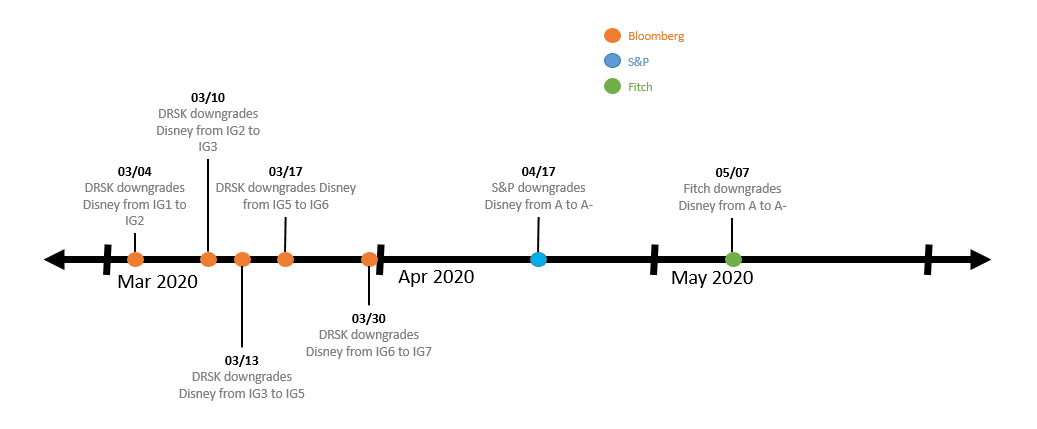

Subsequently, we compared the two-time series. In doing so, we were able to assess how often the DRSK data changed before the rating downgrade occurred, and how much earlier.

We found that during this 100-day period, for the 307 issuers downgraded by two or more notches, the DRSK output produced early warning signals for 90.0% of downgrades, on average 29 days earlier.

These results provide strong evidence of the predictive power of the DRSK model as an early warning indicator of the potential for increased risk and make the case for using DRSK data to complement alternative approaches.

Bloomberg’s Public Company DRSK model uses a hybrid approach, combining the use of both market and scrubbed fundamentals inputs. It aims to combine the timeliness of a market-derived model with the reliability and coverage of a fundamentals approach. As a result, DRSK is able to provide an alternative to both fundamentals and market-based approaches, through a methodology that incorporates both.

In many cases, DRSK data is used in combination with other Bloomberg default risk datasets such as our Market Implied Probability of Default, Credit Benchmark consensus data along with traditional ratings datasets provided by the rating agencies. This allows risk managers to paint a more comprehensive, holistic picture of the credit profile of issuers using multiple dimensions and measures of risk.