Poor liquidity may hamper spread adjustments

As no alternative rate is a like-for-like LIBOR replacement, banks will need to make an adjustment for credit and term differences between the two in order to avoid a value transfer and minimize legal risk. Yet, success depends on there being a deep, liquid market in the successor rate, otherwise valuation discrepancies arise. As more market participants use overnight risk-free rates, liquidity will deepen and spreads will better reflect underlying market transactions.

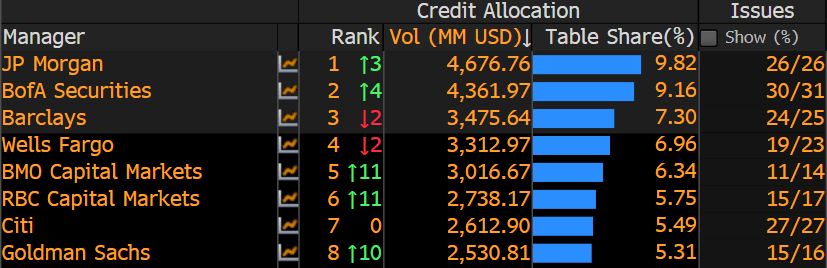

Credit Suisse was the first bank to issue debt linked to the Secured Overnight Financing Rate (SOFR), USD LIBOR’s preferred alternative. Some 906 SOFR-linked bonds were issued in 2020, and 391 in 1Q21. JPMorgan, Bank of America, Barclays, Wells Fargo, BMO, RBC, Citigroup and Goldman Sachs top the Bloomberg manager league table with a 56% market share.