LIBOR Insights

This analysis is by Ira F. Jersey and Angelo Manolatos for Bloomberg Intelligence

LIBOR’s days as a benchmark are numbered, and the secured overnight financing rate (SOFR) remains the most likely replacement in our view - SOFR isn’t a like-for-like substitute for LIBOR since it doesn’t have a credit component. Though challenging and imperfect, we think the transition to the new rate will continue unimpeded.

Regulators have been pushing to replace LIBOR and fed funds as reference-rate benchmarks with a market-based rate that has sustainable volume. While questions still remain on timing and the slow transition to SOFR, the plans are well under way and are moving forward despite COVID-19-related shutdowns and working from home. Some market participants will push back, but regulators’ wishes are likely to win the day. A smooth shift is necessary, so watch for the next steps — because in any transition there are bumps that need to be smoothed out.

The new rate is likely to become ubiquitous, and slow but steady progress has already been made. The addition of New York Federal Reserve-calculated SOFR averages and rate-fallback language for loans, derivatives and securities were major steps in the transition.

Significant progress was made in 2018 and 2019 in the transition to SOFR. Various definitions and fallback language tweaks occurred during 1H20 as well as plans for using the median spread between SOFR and LIBOR as the fallback on existing products after the old benchmark rate is discontinued. The Financial Conduct Authority (FCA) in the U.K. continues to suggest that LIBOR will no longer be published after 2021.

We’re not sure term rates based on SOFR are necessary if current compounding conventions become the market standard, though many market participants are suggesting they’re necessary. As liquidity improves in futures, the next step may be for the New York Fed to calculate a term or forward SOFR benchmark based off derivatives trades. This could be done similarly to how the federal funds rate is calculated.

Though reference rates are used in a wide array of financial products and contracts, the scarcity of underlying transactions in some poses risks to continuity and soundness. With ongoing regulatory reforms and ever-changing market structure, short-term unsecured borrowing may be further eroded, especially during periods of stress. Recognition of these structural risks has prompted the Financial Stability Board (FSB) to take action to identify alternative reference rates.

Along with attempted market manipulation and false reporting, major reference rates such as LIBOR have seen a secular decline in demand for unsecured funding. This structural risk can undermine the certainty and credibility with regard to trading volume, liquidity, pricing and governance.

In response to the Financial Stability Oversight Council (FSOC), the Federal Reserve convened the Alternative Reference Rates Committee (ARRC). This new group of representatives from banks, clearinghouses and the International Swaps and Derivatives Association first met in late 2014 to identify alternative reference rates based on a robust underlying market with strong volume and transaction activity.

The committee was also to take into consideration end users of the rate and its emerging standards, and to enable a smooth transition plan for adopting the chosen alternative reference rate.

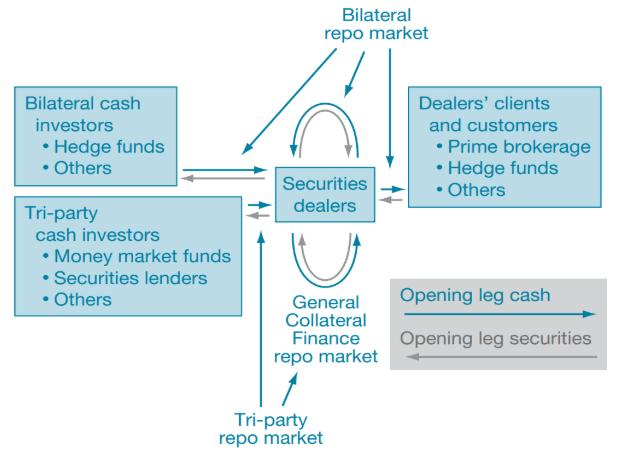

Repurchase agreements are simply a way to borrow funds, usually on a short-term basis, collateralized by securities. More specifically, the lender would transfer cash to the borrower, who will provide a security in return, with the provision that the lender transfer back the original security and interest and that the borrower return the cash plus repo interest at termination. The repo market broadly has three segments: tri-party, bilateral, and general collateral finance (GCF).

In bilateral repo, collateral is exchanged for cash. Tri-party repo involves clearing banks having the responsibility to facilitate repo transactions on their own balance sheet. GCF is an anonymous interdealer market, the transactions of which are settled through the clearing banks.

Source: FRBNY Economic Policy Review