Chapter one

Equipped with algorithms that work much faster than a bank’s human traders, these digital natives have a greater ability to capture small pricing differentials, making them more agile liquidity providers. While Bloomberg’s sell-side bank clients have shown sustained interest in automating their RFQs, COVID-19 has driven an increase in those looking to automate across the entire trade lifecycle. The majority of this interest has come from markets with traditionally cumbersome post-trade processes. In Japan, for example, post-trade workflows are typically more reliant on people being physically present in the office to stamp trade confirms — something that COVID-19 has made particularly inconvenient. Also fueling the shift to automation appears to be a more general trend of trading technology innovation, along with an expected increase in liquidity demands from buy-side customers. Asked to choose the two biggest drivers of fixed income market growth in the APAC region over the next two years, respondents rated the factors of tech innovation and buy-side demands roughly equal in importance. As demand increases, the sell side must respond in kind, with automation of the price discovery process the most likely first step for liquidity providers. Because the quotes themselves are automated, an algorithm can be designed to model the numbers and prices, enhancing overall trading efficiency.

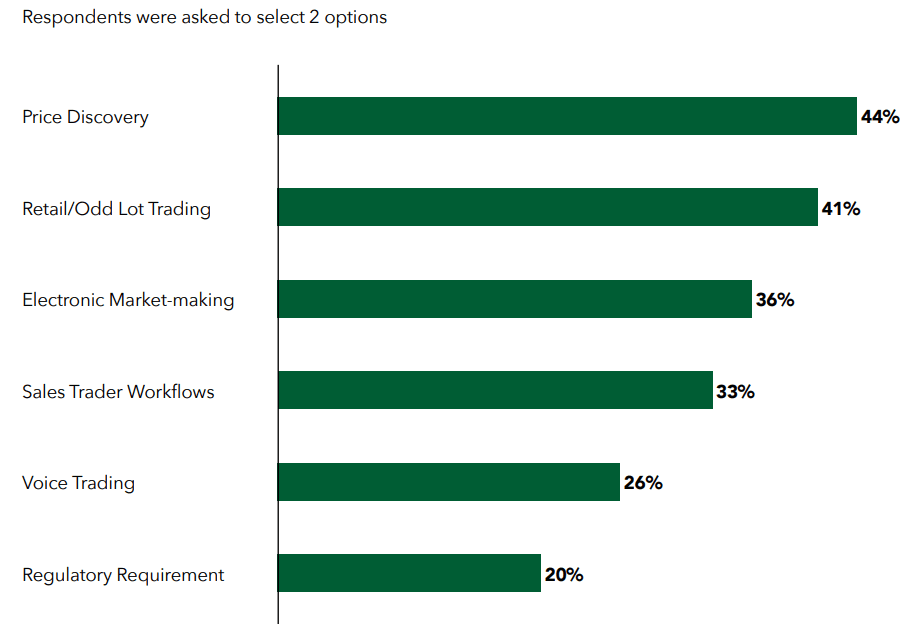

This was closely followed by 41% for retail and odd-lot trading, and 31% for electronic market-making.

Meanwhile, when asked to choose two market making workflow best suited to automation, 44% of respondents chose RFQ response/auto quote, while 38% chose voice response and auto quoting, and 34% chose hedging.

Particularly suited to automation are smaller, everyday trades. As the sell side becomes less reliant on manual processing, this will free up traders’ time to focus on the larger, more demanding trades.

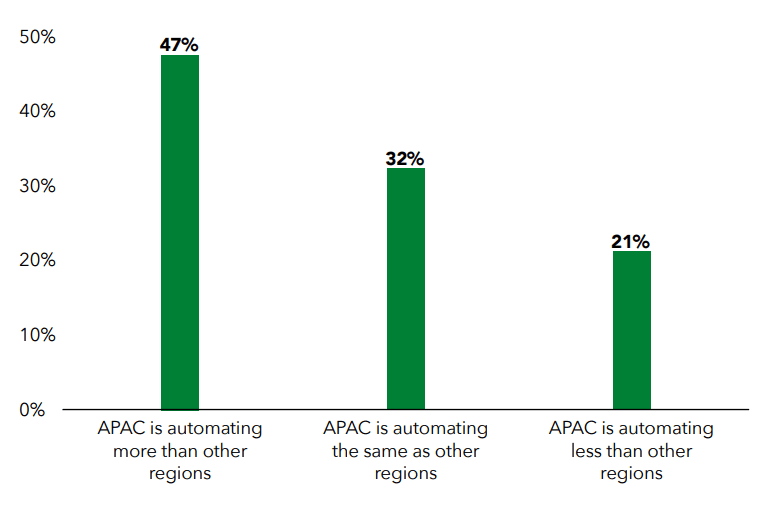

Finally, 32% of respondents said that automation had a greater adoption rate for sell-side fixed income trading in APAC than in North America and EMEA. Although this may be more perception than reality, China in particular is a front-runner in the use and development of AI technology, and there has been an increasing appetite within the region to move away from traditional, telephone-based transactions and implement new automation technology. Analysts have estimated that once the bond futures market has been completely opened up to banks and insurers, this could generate up to $4.2 billion of additional funds and increase the market by as much as 20%.1

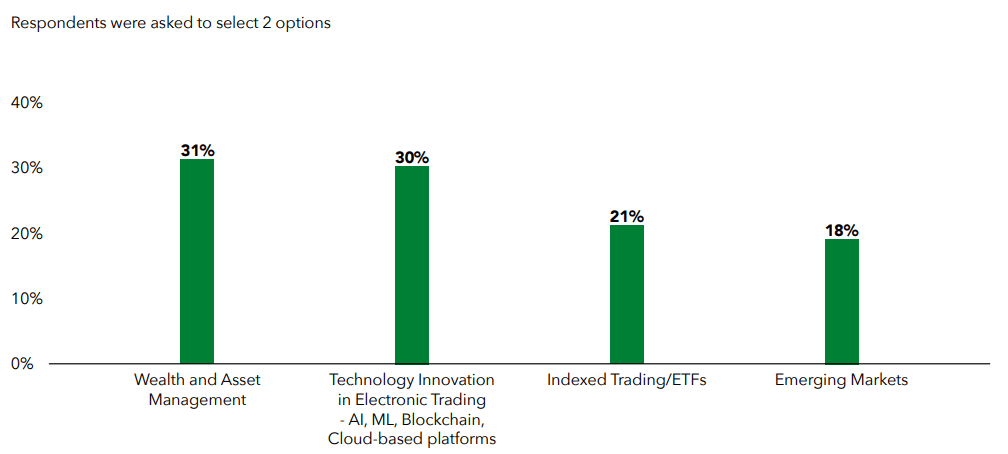

Wealth and asset management and technology innovation in electronic trading are some of the areas that will be the biggest drivers for fixed income market growth in the APAC region in the next two years.

“The buy side has always driven the biggest growth because as their business grow they need greater efficiency. Fixed income has been traditionally very voice-driven, with manual workflows. Electronic trading changed that, but it was the buy side that made it happen and we expect investors to continue shaping technology and market structure innovation.” Dan Tsou, Head of ETOMS, Bloomberg

Price discovery was one of the areas with the biggest demand for automation according to our respondents.

“Retail odd lot trades would be low-hanging fruit and aligns with what we’ve seen. It’s the most obvious part of the business to automate as execution is heavily rule-based and there is enough electronic liquidity to tap into. If you can trade electronically, then being able to automate it becomes the natural next step.” Ravi Sawhney, Head of Trading Automation & Analytics, Bloomberg

“Because price discovery is the first step in the trading workflow, that’s often the first step to be automated. Also, in a universe of millions of bonds, many are equivalent in rating, yield and maturity, but not all are easy to trade, so price discovery helps investors narrow the choices. The other aspect about price discovery that makes a lot of sense is that it’s actually hard work for a sell side trader. If you can automate price setting and dissemination, it helps them do more.” Dan Tsou, Head of ETOMS, Bloomberg

“In Asia, historically, volumes haven’t been as high as Europe and the U.S. Liquidity levels are also not as high, which are the key characteristics to be automating more than the other two. However, when you look at broader-term automation, it does make sense. The region has a culture of innovation and competitiveness, which drives a need to do things more efficiently. I don’t think the real numbers would put Asia ahead, but in terms of intention it’s a very important signal.” Dan Tsou, Head of ETOMS, Bloomberg

“It ties very nicely with the expectation that private wealth will be a major driver of growth. Private wealth trades are comparatively small, or “odd lots”, which are a great candidate for automation. Another thing is the spike in volume. COVID-19 reminded us that if you typically execute 100 trades a day, you need to be prepared for multiples of that when markets spike, because human traders aren’t going to be able to cope.” Dan Tsou, Head of ETOMS, Bloomberg

“When you’ve got a spike in volatility you need the automation machinery to be smart enough to have the option to recognize this and switch the order to manual. From the buy side, the software we provide has a number of checks in place to detect volatility. We saw this result in a greater percentage of orders being executed manually instead of automatically in March. From April, clients started to turn back to automation and in many cases increase their automation rate.” Ravi Sawhney, Head of Trading Automation & Analytics, Bloomberg

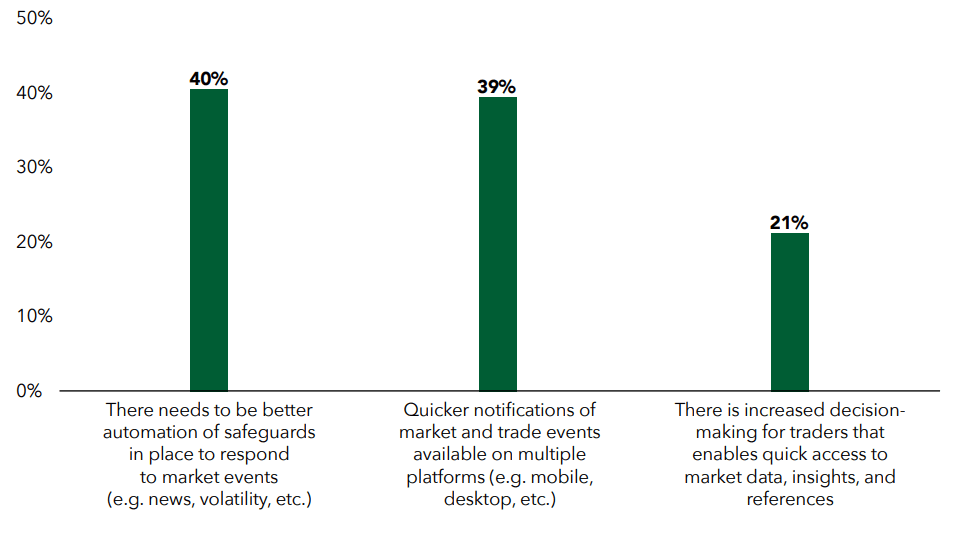

“When you trade by hand, all the safeguards and considerations are part of your trade decision. When you automate these decisions, such as sending automated prices, you have to automate the safeguards as well. Because COVID-19 has created a situation where most people are not currently shouting over the desk to trade, but doing so electronically, we’re seeing a lot more safeguards implemented for their electronic interactions, whether it’s sending out a price, quoting or executing.” Dan Tsou, Head of ETOMS, Bloomberg

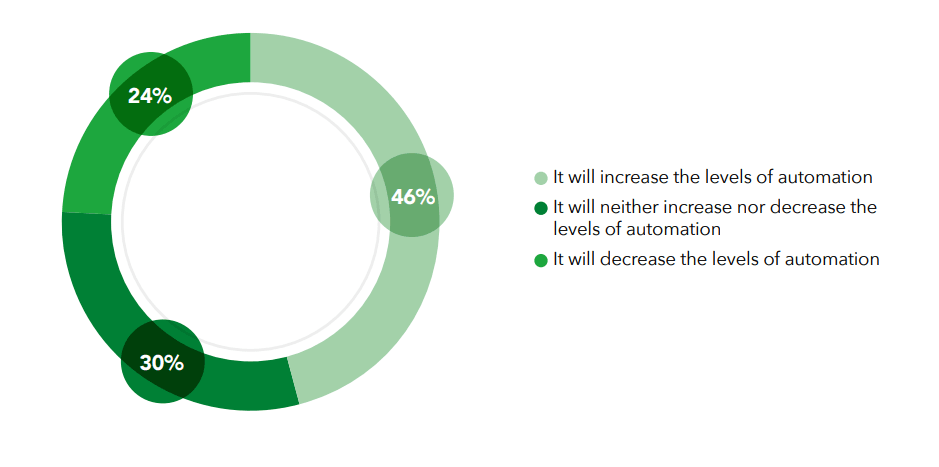

“COVID-19 is clearly acting as an accelerant to the existing trend of increasing automation. When traders are working from home, they’re dealing with other challenges alongside work. They don’t necessarily have the screen real estate they have in the office. They’re dealing with work and home life balance issues. There’s a greater need to augment themselves with technology to help out.” Ravi Sawhney, Head of Trading Automation & Analytics, Bloomberg

“Firms need to improve their ability to support electronic trading because that is going to be the preferred channel when people are dislocated. If you don’t have the right account on the right platform with the right dealer, you may not be able to ask for a price. Firms also need to have the ability to improve safety features by automating volatility signals, liquidity signals, and market signals. Those with the ability to react automatically will come out ahead of those who can only react manually." Dan Tsou, Head of ETOMS, Bloomberg