By BloombergNEF

LNG imports may decline 3.1% from 2019 to 59 million metric tons this year, though the impact on domestic gas production and pipeline imports will be limited. The result will be an exacerbation of the global LNG supply glut which could further drive down spot LNG prices.

Impact on China’s gas demand

Based on a recent Bloomberg survey of economists, China’s economy will likely grow slower this quarter than first thought. The country’s real gross domestic product is now forecast to grow an average of 5.5% for the year. That’s down from an earlier growth forecast of 5.9% for 2020.

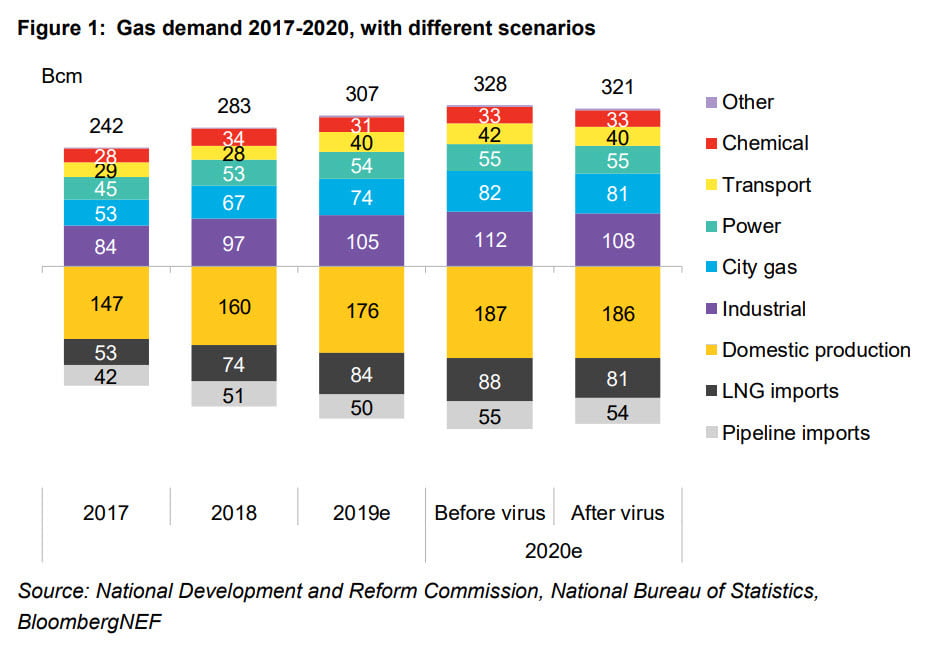

BloombergNEF expects the lower growth outlook to translate to a removal of 7 billion cubic meters of gas demand compared with earlier estimates based on the higher GDP growth outlook. For the year, China’s gas demand will grow just 4.6% to 321 billion cubic meters (Figure 1). BNEF earlier expected gas demand of 328 billion cubic meters in 2020.

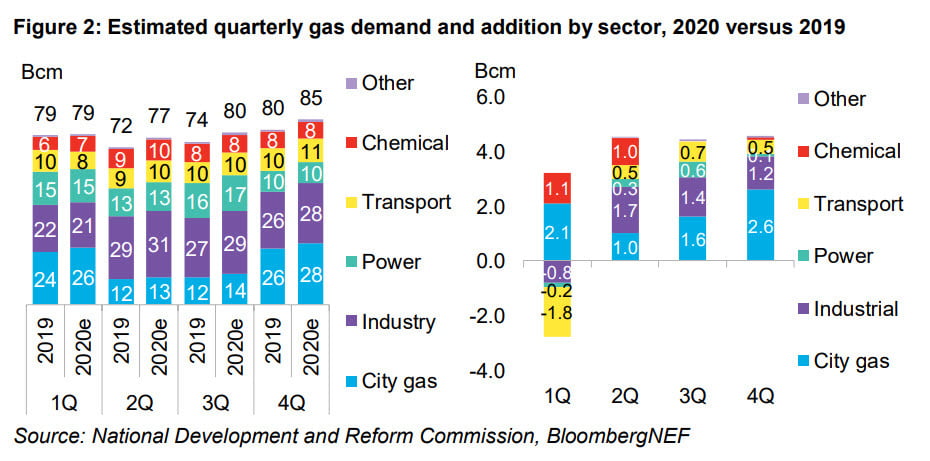

The virus outbreak is expected to result in little year-on-year growth in China’s gas demand in 1Q (Figure 2). This is largely a result of an expected decline in gas usage in the transportation and industrial sectors. The consumption of gas in transport has been dragged down immediately after the Chinese government announced the imposition of travel restrictions and road closures to control the virus spread. Industrial gas demand will decline as factories suspend operations. Two sectors – residential and chemical – will likely see demand continue to grow from 2019 levels. Residential gas demand will likely increase as home heating requirements grow along with people staying at home to avoid the virus. Demand for gas as a feedstock for chemical products such as disinfectants may also surge. However, the growth will not be big enough to pump a year-on-year increase in China’s overall gas demand in Q1.

Gas demand growth will resume in 2Q as virus spread is curbed and the economy recovers. Both industry and power sectors are expected to catch up on growth later in the year as manufacturing recovers to meet annual production targets and power demand rises after the outbreak ends (Figure 2). The government has pledged to introduce a series of measures to boost the economy, including fiscal stimulus, lower electricity/gas/water fees, etc.

While the number of new cases and deaths from the coronavirus outbreak have surged in Hubei province, as China revised its method for counting infections, the Chinese government appears to have contained the spread largely within Wuhan, the province’s capital city. Hubei is home to about 80% of total diagnosed cases in China. Its local economy will be most severely hurt, and gas demand will be slashed there. However, Hubei consumed only about 8 billion cubic meters of gas in 2019 – less than 3% of China’s total gas consumption. Any reduction in Hubei’s gas demand is therefore unlikely to have a significant impact.

Impact on China’s LNG imports

LNG is facing more downward pressure. Even before the outbreak, China’s LNG import growth was already expected to be squeezed by the ramp-up of domestic gas production and faltering gas demand. Now, in addition to the outlook for gas demand being hit by the outbreak’s impact on the economy, control measures have also posed challenges to LNG deliveries.

Delays to cargo discharges can be expected due to limited manpower at terminals and heightened screening of vessels at various ports. Many inter-provincial roads are temporarily closed. Total trucked LNG volumes in 2019 accounted for around 25% of total imported LNG in China. In addition, limited LNG storage capacity, which is already running at high inventory levels, provides little help in dealing with the oversupply caused by the country’s LNG supply contracts and slumping demand.

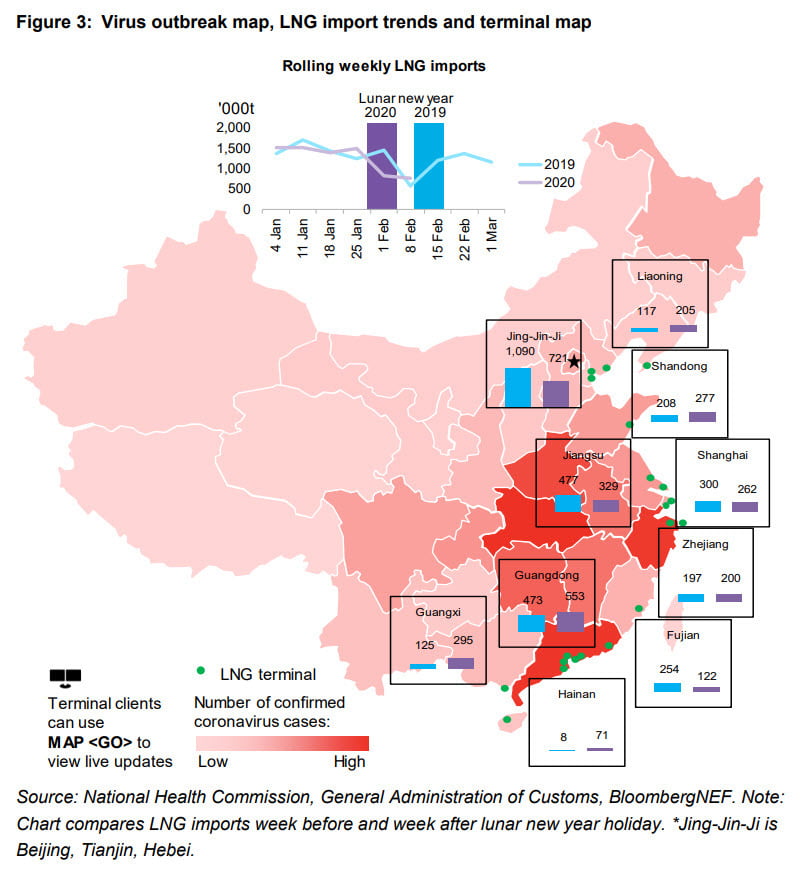

During the holiday period from January 17 to February 7, China’s LNG imports were 7% lower than the lunar new year period in 2019. Hebei, Jiangsu, Fujian, Shanghai, and Tianjin led the drop, with imports falling almost a third (Figure 3).

Chinese buyers are re-routing or rescheduling LNG cargoes due to the virus. In addition, some are trying to declare force majeure to cancel cargoes.

The downward trend will likely continue in the next few months before recovering in Q3 or Q4. Overall, in 2020, China’s LNG imports are estimated to decline 3.1% from 2019 to about 59 million tons. That’s about 5 million tons less than BNEF’s forecast before the outbreak when modest growth was projected.

Impact on international LNG market

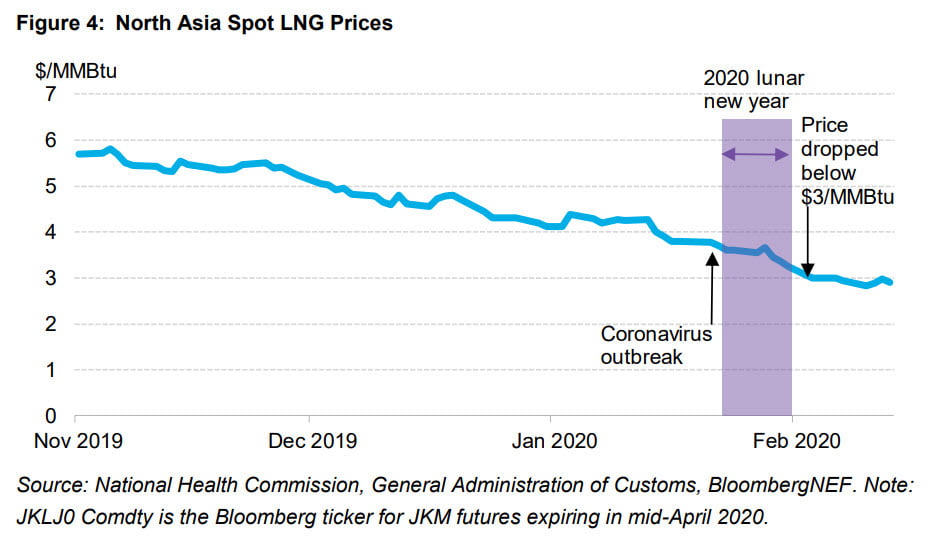

China has become the second largest LNG buyer in the global market since 2017. A softer outlook on China’s total LNG imports will pose a bigger challenge to balancing the already oversupplied global LNG market. Spot LNG prices in Asia have started to reflect the negative impact of China’s virus outbreak on global LNG demand. JKM futures expiring in mid-April fell to $2.95/MMBtu on February 14 from $3.60 on the day Wuhan was closed off on January 23 and the outbreak hit news headlines (Figure 4).

The next few months will be particularly tough for global LNG suppliers. China is expected to experience year-on-year decline in LNG imports, just when North Asia is exiting from winter heating season and European gas system is using up its demand flexibility to respond to low prices. Prices will drop further, and LNG suppliers are set to face an unprecedented high risk of production curtailment.