From a credit risk perspective, not all industries have navigated their way through the crisis equally. While some sectors fared better than others, transportation, energy, tourism, hospitality, and retail have been among the most severely impacted by travel and social-distancing restrictions, raising concerns regarding the solvency and viability of the individual firms in these sectors. In stark contrast, sectors like e-commerce, logistics and technology not only survived but thrived through the pandemic, enabling banks to easily justify, and even expand, the supply of credit to these sectors.

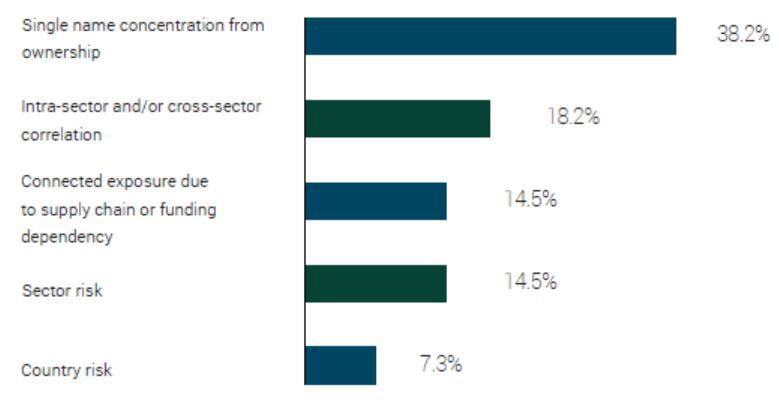

Recognising the uneven impacts of the pandemic on specific industries, almost a third of respondents (32.7%) pointed to sector risk, as well as intra-sector and cross-sector correlations, as considerations in their measurements of concentration risk. For parts of the economy that were more severely impacted by the pandemic, banks put in place stricter limits around sector concentration risk, in many cases demanding higher quality collateral and imposing additional terms in loan agreements.

“The pandemic gave us justification to go back and tighten up contractual certainty with trading counterparties, specifically corporates,” said the head of financial market credit exposure management at a European bank in Singapore. “In Asia, most of the time you don’t have a CSA [credit support annex] with corporate clients. We were able to negotiate CSAs with many of