By Elchin Mammadov, Bloomberg Intelligence

This article is also by contributing analyst Talon Custer from Bloomberg Intelligence.

China imposing higher tariffs on U.S. LNG could help rival exporters (Qatar Petroleum, Woodside Petroleum, Gazprom, Novatek), commodity traders (Gunvor, Trafigura, Vitol), diversified portfolio players (Shell, Total, Chevron, Exxon) and possibly European utilities (Centrica, Naturgy, Engie).

This article is also by contributing analyst Fernando Valle from Bloomberg Intelligence.

Sempra-Aramco deal shows LNG market is fluid despite trade war

Sempra's deal with Aramco underscores how it's still possible for U.S. developers to build new LNG projects by signing long-term offtake agreements with non-Chinese buyers, despite the U.S.-China trade war. The U.S. company has already signed binding agreements with Poland's PGNiG, and non-binding deals with Saudi Aramco, Total, Tokyo Gas and Mitsui. Sempra will probably pursue more non-China offtakers, including Kogas. The U.S. company may reach a final investment decision on its Costa Azul Phase 1 LNG project this year and on Port Arthur Phase 1 by 2020, in our view, based on progress to date. First gas deliveries will be due by 2023 and 2026, respectively.

Trade war may strengthen non-U.S. exporters of LNG

The U.S.-China trade war may force Venture Global, Sempra, Kinder Morgan and other LNG project developers in the U.S. to look outside China for alternative long-term contracted gas buyers, which would have enhanced bargaining power. Otherwise, U.S. exporters may decide to sell their gas on the global LNG spot market, which would increase their exposure to price and volume risk. If Chinese buyers keep shunning long-term deals with U.S. LNG exporters, it would strengthen the position of Novatek, Gazprom, Qatar Petroleum, Woodside and other rivals outside America seeking to sign long-term deals to expand their LNG export capacity.

Traders, oil majors, EU utilities could be winners

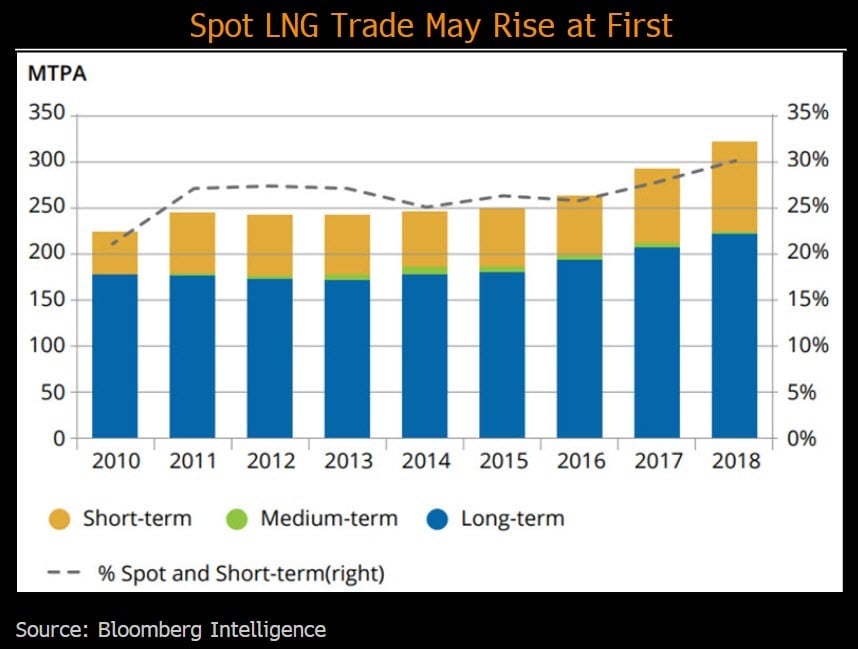

China's decision to increase tariffs on LNG coming from the U.S. may increase the share of spot and near-term LNG trading globally, as Chinese buyers swap U.S. gas imports for LNG cargoes originating from Qatar, Australia, Russia and other geographies. This could benefit commodity traders (Gunvor, Trafigura, Vitol), portfolio players (Shell, Total, BP, Chevron, Exxon), and European utilities (Centrica, Naturgy, Engie, EDF, PGNiG). These companies have access to non-U.S. cargoes, and they may be able to charge Chinese importers a price just below the cost of delivered U.S. LNG, including a 25% tariff premium. The absence of competition from Chinese buyers may also allow European utilities to command increased bargaining power when negotiating long-term LNG offtake deals with U.S. gas exporters.