The implications of time

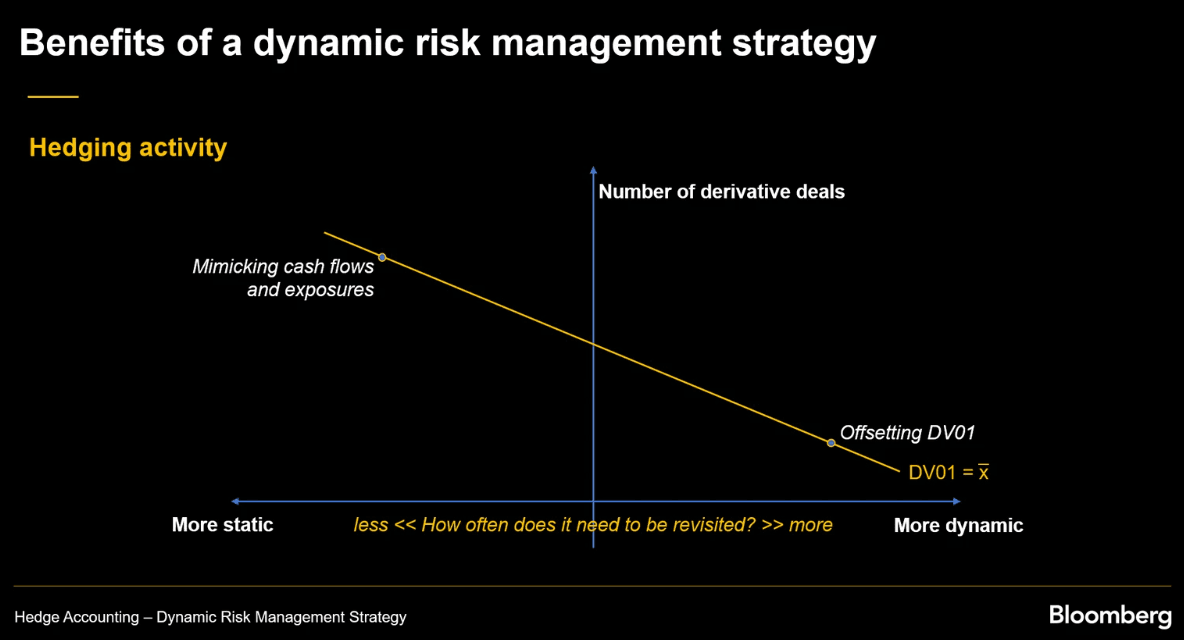

From the perspective of a single snapshot in time, it seems obvious that hedging via DV01 offsetting is much more efficient than trying to offset individual exposures and cash flows. However, it is also vital to understand how these hedging strategies function over time.

The first time-related aspect to consider is the sensitivity of the sensitivity: a second order measure known as the gamma measure. The gamma measure allows risk managers to evaluate changes in the delta with respect to changes in the interest rate curve.

Based on this measure, an individually hedged portfolio will perform rather well. This is because, as time passes, the risk structure from both the exposures and hedges will evolve in tandem, alongside their own delta measures. There would be no need to make any changes to the relevant derivatives.

On the other hand, a dynamic approach that uses a single swap to offset DV01 would probably fare rather badly when trying to offset Gamma. After a few weeks or months, if not days, the swap would fail to stabilize the net interest rate margin. It would require constant monitoring and revisiting by adding more swaps.