A comprehensive pricing library

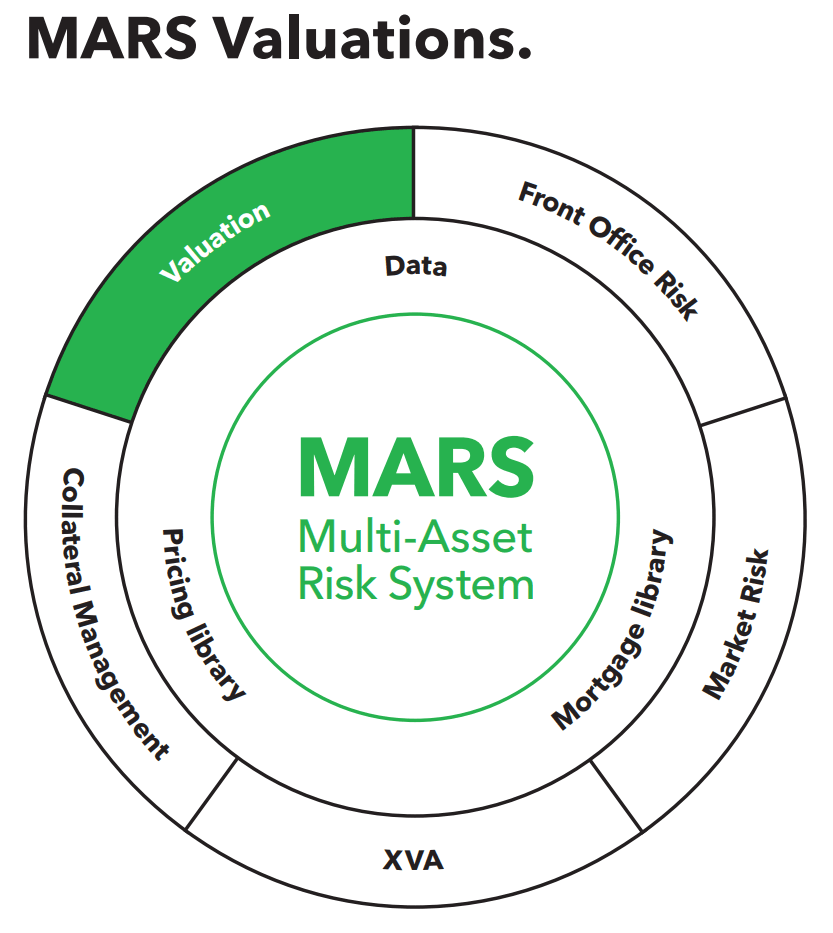

In evolving markets with increasing regulatory oversight, both buy-side and sell-side firms need a powerful solution to value their portfolios and understand their key risks. Using comprehensive pricing library and market-leading Bloomberg data, MARS Valuations solution delivers credible and comprehensive end-of-day market values and Greeks for your entire portfolio for enterprise use with a powerful, versatile and highly intuitive experience.

Broad coverage, flexible pricing

Bloomberg’s MARS function has comprehensive asset class coverage for valuations and encompasses a broad spectrum of financial instruments. MARS provides you full transparency into, and flexibility with, market data and pricing models.

The right model for your needs

Bloomberg MARS Valuations is built on a comprehensive quantitative library that offers a range of pricing models. Whether you are pricing typical treasury contracts such as vFX forwards & options, vanilla & cross currency interest rate swaps or more complex products such as real rate swaps, FX baskets or a long dated FX-IR hybrid, the pricing library provides the right modeling technique to capture the market dynamics. The list of models includes but is not limited to local volatility, stochastic volatility (such as Heston Model), stochastic local volatility, Hull-White one-two-factor, shifted Libor market model, hybrid Hull-White one-factor and local volatility.

Market-leading data

As industries become more aware of the hidden complexities within financial products, high-quality underlying market data is playing an ever-more-prominent role. Bloomberg employs innovative data-cleaning techniques and algorithms to generate high-quality data. MARS Valuations enables you to feed high quality Bloomberg data and snapshot-based golden data into its state-of-the-art pricing library to derive valuations for enterprise use.